Mobile Virtual Network Operator Industry Overview

The global mobile virtual network operator market size is expected to reach USD 109.9 billion by 2027, registering a CAGR of 7.6% from 2020 to 2027, according to a new report by Grand View Research, Inc. The growing demand for data services and increasing number of mobile users across the globe is expected to drive the market. In addition, the increasing number of services such as cloud, Machine to Machine (M2M), and mobile money are further expected to drive demand for mobile virtual network operators over the forecast period.

The growing demand to access mobile applications, social media, and multimedia services is further expected to propel the growth of the market over the forecast period. The declining prices of smartphones are contributing to the accelerating subscriber penetration across the globe is expected to fuel the growth of the market. Furthermore, increasing partnerships formed by key players for providing high-speed data services to consumers is anticipated to drive market growth over the forecast period.

Mobile Virtual Network Operator Market Segmentation

Grand View Research has segmented the global mobile virtual network operator market on the basis of type, operational model, end use, and region:

Based on the Type Insights, the market is segmented into Business, Discount, M2M, Media, Migrant, Retail, Roaming, Telecom.

- The market is expected to witness significant growth in the M2M market due to the increasing adoption of cellular connectivity in machines ranging from vehicles to vending machines.

- Technical advancements in the 3G M2M market, an extension of mobile network coverage, and initiatives by MNOs to expand their service offerings are the key factors supporting the growth of MVNOs in the M2M market.

- There has been a significant increase in the number of MNOs collaborating with M2M application service providers, which is expected to drive the demand for mobile network element deployment in M2M applications over the forecast period.

- MNOs offer various service plans and products for different markets having fewer users, which leads to expensive and inefficient operational and business support systems. The cost associated with retaining and acquiring new customers is relatively high, mainly for fixed term contracts.

- The mobile virtual network operators can help in overcoming cost issues, optimizing resource allocation, and improving the Quality of Service (QoS). This, in turn, would contribute to the growth of the market for mobile virtual network operators.

Based on the End-use Insights, the market is segmented into Consumer, Enterprise.

- The consumer segment dominated the market for mobile virtual network operators in 2019 and is expected to maintain its dominance over the forecast period.

- The mobile virtual network operator model offers benefits such as time efficiency and cost-effectiveness, which is expected to lure more consumers, in turn, accelerating the growth of the consumer segment.

- Managing connected living, personal data, and rising e-commerce activities is also anticipated to provide significant growth opportunities for key players operating in the market for mobile virtual network operators along with increasing consumer benefits.

- The mobile virtual network operators model is shifting from voice to a more data-centric experience. MVNOs across the globe are looking for data-capable smartphones as a way to expand their businesses.

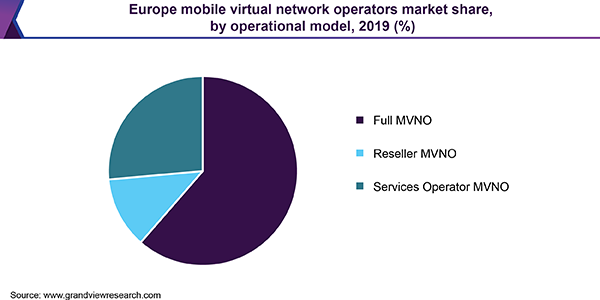

Based on the Operational Model Insights, the market is segmented into Full MVNO, Reseller MVNO, Service Provider MVNO.

- The full MVNO segment dominated the market for mobile virtual network operators in terms of revenue in 2019. Implementation of full MVNO network infrastructure requires low capital investment and gives full call control, which allows customers to call internationally at highly discounted rates.

- The emergence of mobile virtual network operator is the result of regulatory interventions to lower the barriers for entry and eventually increase competition and strategic decisions undertaken by MNOs.

- MNOs have their own mobile licenses, infrastructure, and customer relationships with their end users and are capable of handling network routing. They generally have roaming deals with foreign counterparts.

- They are aiming at capitalizing opportunities related to roaming services by providing special services to tourists and youth. MVNOs aid in increasing revenue for MNOs by providing wholesale deals, increasing network utilization, and creating their MVNO’s by launching sub-brands.

Mobile Virtual Network Operator Regional Outlook

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa (MEA)

Key Companies Profile & Market Share Insights

Industry players are also adopting various strategic initiatives such as partnerships, mergers and acquisitions, collaborating with other firms for gaining a competitive edge and deploying better services to their customers.

Some prominent players in the global mobile virtual network operator market include

- Lebara Group

- Lyca Mobile

- TalkTalk Group

- Giffgaff

- Poste Mobile SpA

- Virgin Mobile

- TracFone Wireless Inc.

Order a free sample PDF of the Mobile Virtual Network Operator Market Intelligence Study, published by Grand View Research.

About Grand View Research

Grand View Research, U.S.-based market research and consulting company, provides syndicated as well as customized research reports and consulting services. Registered in California and headquartered in San Francisco, the company comprises over 425 analysts and consultants, adding more than 1200 market research reports to its vast database each year. These reports offer in-depth analysis on 46 industries across 25 major countries worldwide. With the help of an interactive market intelligence platform, Grand View Research Helps Fortune 500 companies and renowned academic institutes understand the global and regional business environment and gauge the opportunities that lie ahead.